The Geopolitical Undercurrent in Critical Mineral Value Chains: Africa’s Emerging Leverage as a Wildcard in Resource Scarcity

Exploring an under-recognised geopolitical wildcard in critical minerals: Africa’s latent capacity for reshaping global supply chains and industrial strategy beyond mere resource availability.

Resource scarcity debates around critical minerals increasingly focus on supply volume and substitution technology. However, a less visible but structurally potent wildcard is Africa’s burgeoning strategic leverage, driven by its vast mineral deposits, renewable energy potential, and demographic dynamics. Unlike conventional narratives that frame Africa principally as a resource periphery, this paper identifies a geopolitical inflection poised to recalibrate capital flows, regulatory paradigms, and industrial architectures over the coming two decades. The underlying shift is not solely supply-side expansion but emerging African leverage within a fragmented global trading system seeking green industrialization and resource security.

Signal Identification

This development qualifies as a wildcard because it remains largely underappreciated in mainstream critical mineral supply discourse, which tends to prioritise existing dominant producers and shift supply-chain footprints to China, the US, or Europe. Africa’s strategic centrality—as a nexus of critical mineral reserves, clean energy potential, and a youthful labor pool—has significant leverage power that is nascent but plausible to materialize within a 10–20-year horizon. The plausibility band is medium, given geopolitical uncertainties and infrastructural constraints, but is grounded in credible policy developments and resource endowments. Key sectors affected include mining and refining, green energy technologies, global manufacturing, and geopolitical risk governance in commodities.

What Is Changing

Multiple intersecting trends reveal Africa’s rising strategic profile beyond historical extractive roles. Africa possesses vast reserves of metals critical to the global green transition such as cobalt, lithium, and rare earth elements (TessForum 26/06/2026). These minerals are foundational for batteries, electric vehicles, renewable energy systems, and defense technologies. Yet, what distinguishes the African signal is not mere resource availability but the geopolitical and industrial repositioning underway.

First, African governments and regional blocs are reclaiming policy space traditionally ceded to global commodity markets, pushing for green industrialization pathways that integrate mining with domestic value addition and renewable energy infrastructure (ibid). This challenges the conventional extractivist model dominated by Western or Chinese firms, disrupting global industrial structures and prompting rethinking of capital allocation strategies.

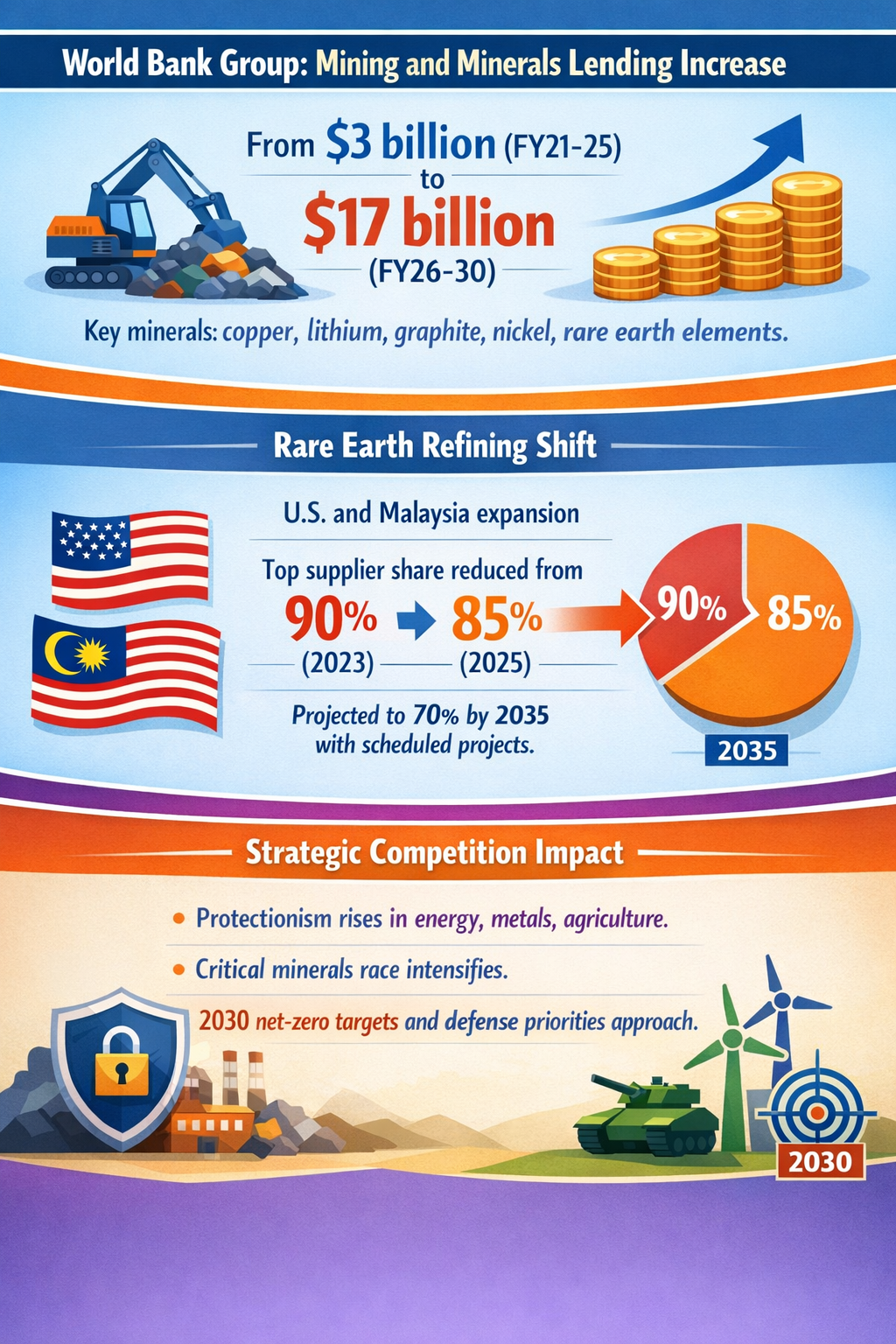

Second, the strategic competition in critical minerals amplifies protectionist tendencies, with superpowers wary of supply concentration risks (Financial Times 01/07/2026). Africa’s increasing political agency and potential to harness its renewable energy advantage—critical for low-carbon refining and processing—introduces a leverage point that may reroute investment flows and alter regulatory frameworks from resource security standpoints.

Third, African mineral projects are starting to fulfill significant demand requirements in advanced economies. For instance, South Africa’s rare earth processing facilities could supply one-fifth of Europe’s demand, including heavy rare earths vital for magnets critical to clean energy devices (Carnegie Endowment 26/06/2026). Similarly, new mining projects like the Rovina Valley in Europe are positioning to attract African-linked capital and expertise, pointing to emerging regional supply co-dependence (GlobeNewswire 26/06/2026).

Fourth, the recent reduction in Chinese dominance in rare earth refining—declining from 90% market share in 2023 to a projected 70% by 2035—may open opportunities for African partnerships or alternative supply chains outside existing Sino-Western bipolar frameworks (IEA 15/05/2026). Considering China's past efforts to wield critical mineral leverage in geopolitical disputes (Foreign Affairs 12/04/2026), Africa’s ascendancy as an independent or allied supply node could recalibrate global leverage balances.

Disruption Pathway

Africa’s emergent leverage could unfold structurally if a combination of enabling conditions accelerates. These include enhanced governance frameworks enabling investment stability, infrastructure development powered by renewable energy (to address energy-intensity and emissions concerns in mining/refining), and strategic regional integration promoting economies of scale in value addition.

Pressure from Western and Asian actors to diversify supply may catalyze capital influx into African upstream and midstream mineral processing, creating industrial clusters that reduce dependency on established chokepoints. This would stress incumbent governance and market systems that currently centralize trade flows around a narrow set of players. African policy autonomy and industrial policy could provoke re-trading of geopolitical alliances and reshape global supply chain governance.

Structural adaptations may include the rise of pan-African commodity regulatory bodies emulating European strategic frameworks (drawing on the EU’s approach with projects like Rovina Valley) and cross-border energy grids facilitating low-emission mineral processing. Feedback loops could emerge as increased African agency raises commodity price volatility by inserting new political risk dimensions, thereby prompting further diversification strategies by downstream manufacturers.

Unintended consequences might include fragmented global critical mineral markets, rival blocs competing for African partnerships, or internal African political-economic tensions reconfiguring resource governance. A successful African strategic industrialization could lead to a dominance shift away from current triadic supply chain hegemons (China-USA-EU), demanding new regulatory models internationally. This evolution may also accelerate digital traceability and sustainability standards, as African producers seek preferential market access.

Why This Matters

For capital allocators, recognizing Africa’s growing strategic leverage implies a possible redirection of investments from purely volume-driven extraction projects toward integrated green industrial clusters that blend raw material extraction with processing and renewable energy generation. This could reconfigure risk-return calculations and raise the importance of political risk analysis informed by African governance trajectories.

Regulators and policymakers face the prospect of revising trade and investment frameworks to accommodate African industrial policy ambitions, including mechanisms to incentivize value addition and emissions reductions. Competition law, export controls, and green industrial policies may need recalibration to address emergent multi-polar supply systems rather than binary resource nationalism.

Industrial actors positioned within current supply chains must anticipate new African actors not merely as suppliers but as strategic partners or competitors capable of redefining pricing power, sustainability credentials, and technological innovation pathways. Supply chain resilience assessments should incorporate African political economy as a critical dimension.

Governance bodies charged with security and defense technologies must consider African rare earth processing capacities within strategic risk frameworks, recognizing the continent’s potential role in decoupling scenarios or bloc-based supply realignments.

Implications

This scenario may lead to structurally diversified and more multipolar critical mineral markets, reducing systemic risks associated with concentration in a handful of countries. Capital flows could increasingly target downstream processing and renewable electrification projects in Africa, potentially fostering new industrial ecosystems.

However, this signal is not guaranteed to result in transformative shifts. Constraints such as infrastructural deficits, political instability, and global financial conditions might stall or confine African leverage to niche roles. Competing interpretations regard Africa as perpetually disadvantaged by these factors, limiting its capacity to influence global industrial structures.

The emergence of African leverage should not be conflated with simplistic resource nationalism or extractive expansionism. It involves sophisticated industrial policy, regional cooperation, and geopolitical agency that might recalibrate global resource governance with sustainability and development objectives intertwined.

Early Indicators to Monitor

- Surge in venture and infrastructure capital directed toward integrated mineral processing and renewable energy projects in Africa.

- Formation of pan-African or regional regulatory bodies governing mineral exports with binding sustainability and value addition mandates.

- Significant shifts in trade and diplomatic agreements featuring Africa’s critical mineral sectors as strategic assets.

- Public-private partnerships demonstrating co-development of downstream clean energy or battery manufacturing linked to African minerals.

- Policy announcements and funding streams from multilateral institutions prioritizing African critical mineral industrialization aligned with green transition.

Disconfirming Signals

- Persistent or worsening political instability and conflict in key mining regions undermining investor confidence.

- Stalled infrastructure development or failure to electrify mineral processing activities with renewable energy.

- Dominance re-consolidation by existing refining hubs (e.g., China) with significant cost or logistical advantages retained.

- Lack of credible African institutional cohesion or policy continuity to support strategic industrialization.

- Global demand shocks or technological breakthroughs reducing critical mineral dependency substantially.

Strategic Questions

- How should governments and investors assess African policy autonomy risk in emerging critical mineral industrial clusters?

- What regulatory and partnership models will best support equitable, sustainable value chains that embed African resource sovereignty?

Keywords

Critical Minerals; Resource Scarcity; Geopolitical Risk; Green Industrialization; Africa; Renewable Energy; Supply Chain; Rare Earth Elements

Bibliography

- Africa has become strategically central to the global green transition owing to its vast reserves of critical minerals, significant renewable energy potential, and youthful labour force. TessForum. Published 26/06/2026.

- Strategic competition is reinforcing protectionist approaches across energy, metals and agriculture, while the race for critical minerals is accelerating as 2030 net-zero targets and defence priorities draw closer. Financial Times. Published 01/07/2026.

- Chinese officials forced the Trump administration to lift U.S. tariffs on Chinese products by threatening to cut the United States off from critical minerals. Foreign Affairs. Published 12/04/2026.

- In rare earth refining, new projects in the United States and production increases in Malaysia reduced the share of the top supplier from over 90% in 2023 to 85% in 2025, and if planned projects come online as scheduled, it is projected to fall to 70% by 2035. International Energy Agency. Published 15/05/2026.

- Most important is South Africa's rare earth extraction and processing facility, which could fulfill about one-fifth of European demand (including for heavy rare earths). Carnegie Endowment. Published 26/06/2026.

- Already granted European strategic status, the Rovina Valley Project is expected to unlock much needed investment and job creation in Hunedoara County and will deliver critical minerals necessary for Europe's green energy transition. GlobeNewswire. Published 26/06/2026.